Guided scheme design

Vestd provides UK companies with a fully guided service for share and option schemes. You’ll always get five star support. Get started by booking a free consultation.

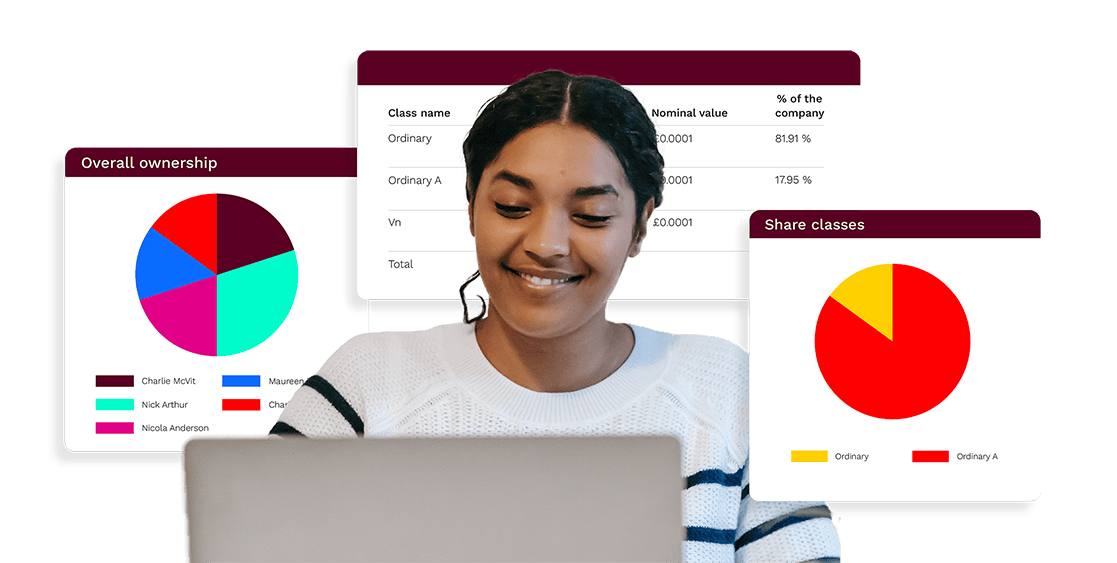

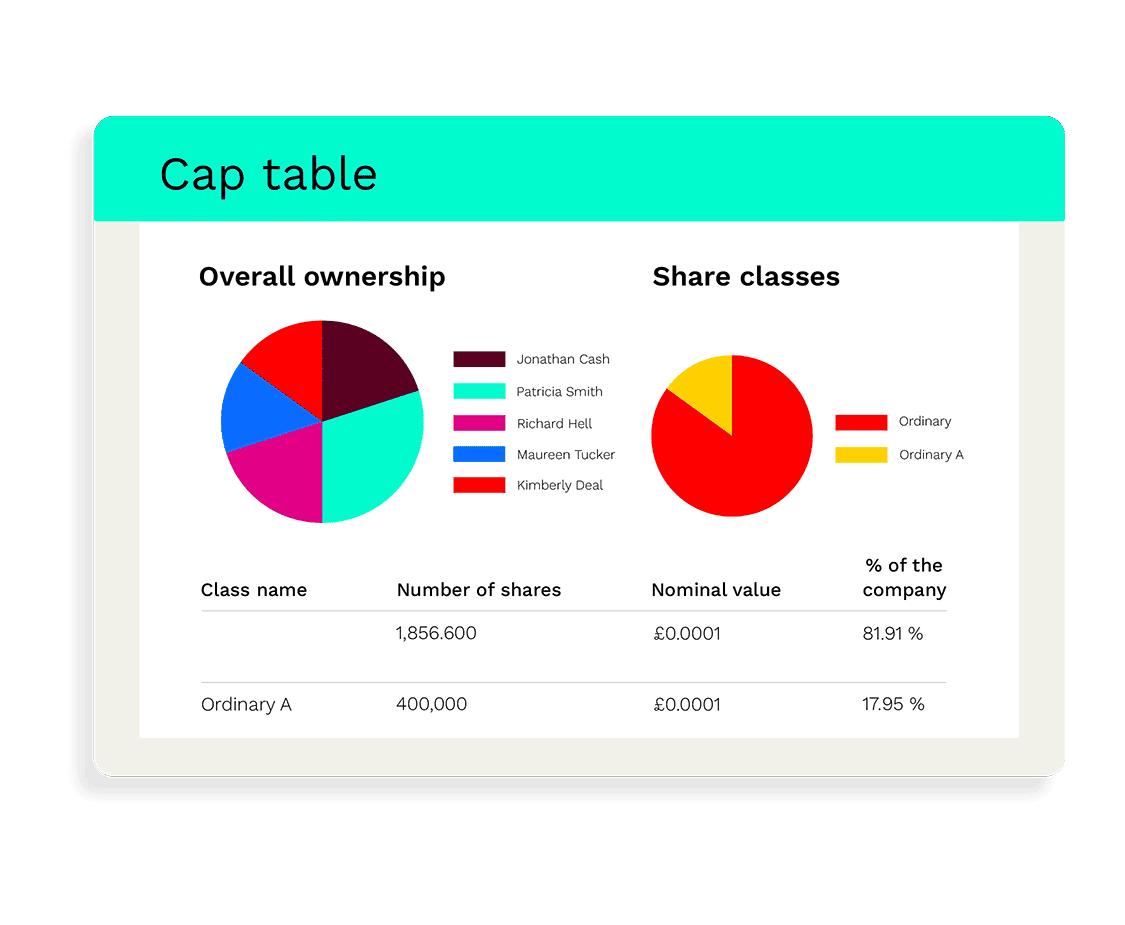

Manage your equity and shareholders

Share schemes & options

Fundraising

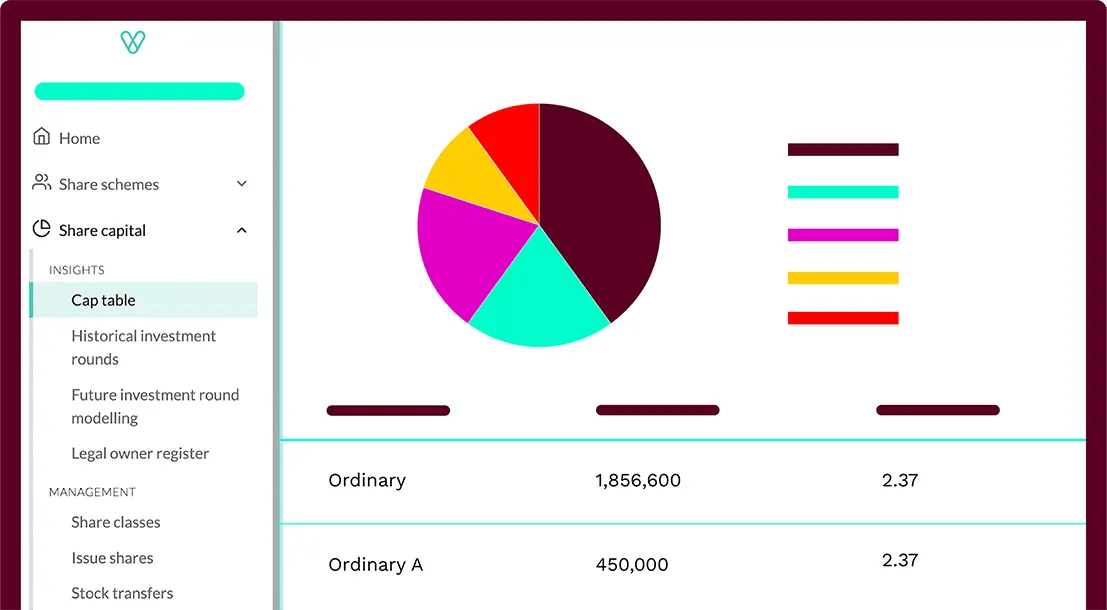

Equity management

Start a business

Company valuations

Launch funds, evalute deals & invest

Special Purpose Vehicles (SPV)

Manage your portfolio

Model future scenarios

Powerful tools and five-star support

Employee share schemes

Predictable pricing and no hidden charges

For startups

For scaleups & SMEs

For larger companies

Ideas, insight and tools to help you grow

There are no statutory requirements or limits to abide by so these options can be granted very quickly.

✓ Ideal for non-employees

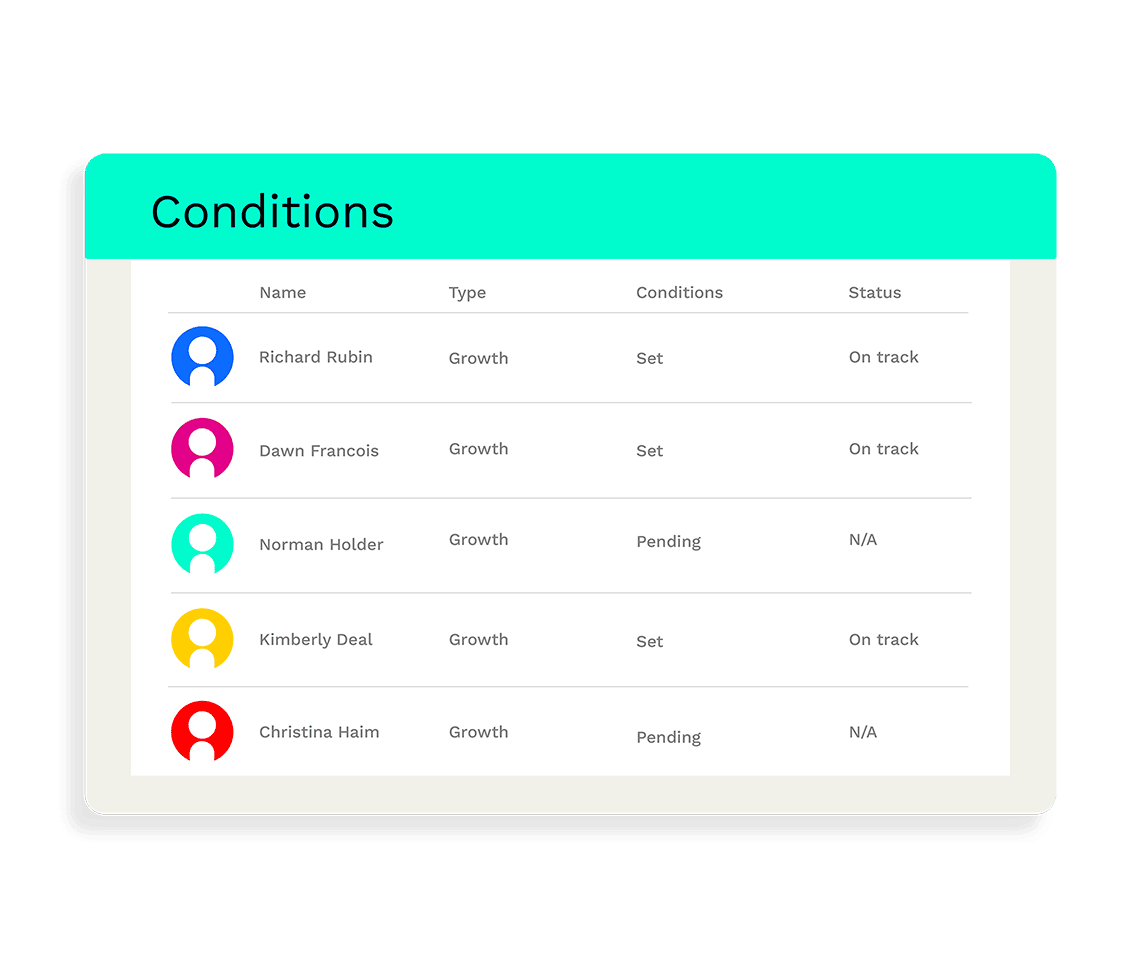

✓ All sorts of conditions can be set

✓ Can be used internationally

There are more tax efficient ways to give people skin in the game but unapproved options are about as flexible as it gets.

✓ Don’t need a formal valuation for HMRC

✓ Can be granted below market value

✓ Cost of the scheme can be offset

You can set conditions for recipients, such as achieving milestones, or staying with the company for an agreed period of time. We’ll help you figure out the best conditions - what’s most important is that the criteria is clear and not subjective.